The Shared Transaction Repository

(STR) Accountant's explanation

|

Home |

Below is tutorial aimed at accountants and

bookkeepers, showing how shared data on the Internet can improve

accounting processes.

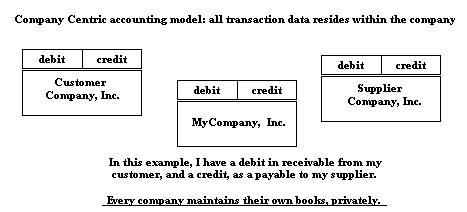

This is not an automatic reconciliation or

replication scheme. The STR is a true shared

database. It is a true shift from company-centric to

a single, shared, network-centric storage and transaction execution.

| 1950-2000:

Debits equal Credits in my ledger.

- CDEA -classic double entry

accounting

- benefits internal bookkeeping

- administering

external balances requires continual work.

|

|

| Web applications - more of the same:

Debits equal Credits in my ledger.

- more CDEA.

- same benefits in internal bookkeeping

- no benefits in administering

external balances.

|

|

| Future, abstract:

Debits equal Credits within each trade, globally, among trading

partners.

- external balances are kept in

balance

- the root ledger of the

enterprise is not defined or constrained (legacy system can

continue.)

(This model is nuts

because the debits and credits that have floated up, are equal. See

the next frame.) |

|

|

Single record of each trade, meeting

the needs of both trading partners symmetrically

- single entry

accounting

- works fine for consumers.

- general ledger is not provided

yet.

- but we have accomplished a good

thing: we have converged the AR and AP amount and date,

and description.

|

|

|

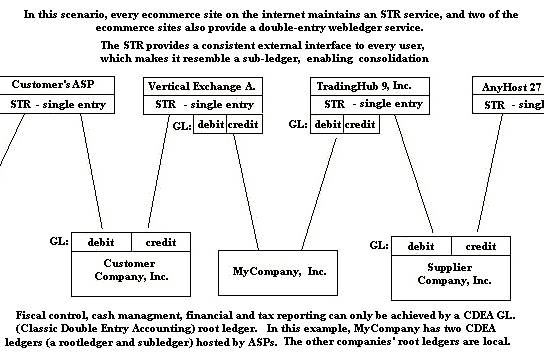

Future, STR model:

- ASPs and BSPs begin to provide persistent

storage

- You might call this NSEA - Network single entry

accounting. Only records of transaction events are

stored.

-

general ledgers may be maintained locally or on hosts or ASPs.

- combining of general ledgers

follows conventional consolidation methods.

- general ledgers may contain

replicas of STR entries, or just pointers.

|

|

|

Future Scenario:

triple entry accounting

- ASPs and BSPs provide persistent STR structures

- Triple entry accounting. Records of transaction events are

stored, with private stub space, for party's use

-

The host is your general ledger, or sub-ledger.

- Your root ledger can contain

replicas of every transaction, or summary entries with pointers

and indexes.

|

|

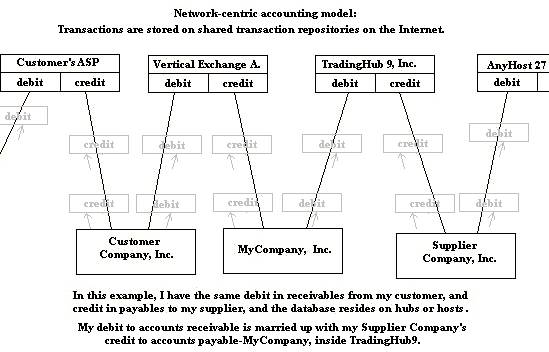

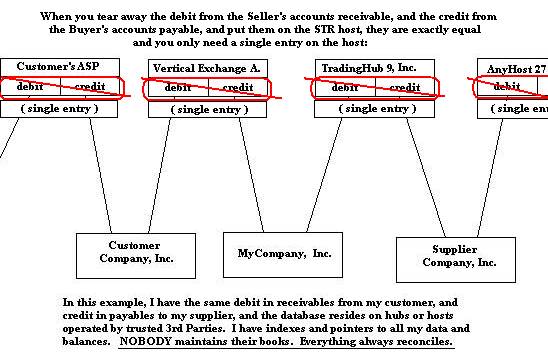

Note that in network-centric accounting,

- the pairs of debits and credits reside on hosts where

exchanges were mediated or transported, rather than inside the ledgers of the trading

partners.

- those pairs of debits and credits are not the same ones

that

would have been recorded inside the company-centric ledgers. There is

a debit from one party and a credit from the other.

- the pairs of debits and credits are

resolved into a single event record. The single record

contains the parties' identity, date, amount, and the consideration,

etc.

- each party donated a debit or a credit-- they

still need the other half of those CDEA entries.

Accordingly, STR is a triple-entry system providing a private stub for

each party's balancing entry. Most

businesses will continue to maintain classic double-entry ledgers as

in the past. But they don't have to: they can store those

on the servers, too, explained below.

But first, let's take a break, and get beat up by the small business

owner.

| |

"The objective of this architecture is to achieve the

simplest possible scheme for shared storage of transactions that

eliminates redundant storage, and eliminates any possibility of

inconsistency between the parties' records. " |

|

|

"Yeah right. I am going to store my

general ledger on your computer, on the internet? " |

|

| |

"No. You are going to store only

the date, amount, and description of your transaction

events on the internet,

encrypted so that only you and your trading partner can ever read

them. " |

|

|

"Why that's ridiculous. Why should I share any

of my data with my customer or supplier? " |

|

| |

"You already do. A snapshot of whatever you

bought or sold, or agreed upon, will be stored. Your

customer or supplier already stores the exact same information, internally.

Whatever you agreed upon is exactly the same information. " |

|

Alternatives to consider:

A shared transaction repository could be achieved using any high-end multi-company

accounting system. You could record classic, double-entry accounting

(CDEA) transactions within such a ledger

for each party, just as intercompany transactions have been formed within

controlled groups, for the last 100 years. Consider this example

where Subsidiary A pays an expense for Subsidiary B thru "the

intercompany account".

General Ledger - Subsidiary

A

July 2000

JournalNo. Date LineNo.

Account

Amount

4441 22/7/2000 531

10100 Cash in Bank Cr

-400

4441 22/7/2000 532

19000 Interco Receivable Dr 400

...

.. |

General Ledger - Subsidiary

B

July 2000

JournalNo. Date LineNo.

Account

Amount

73821 2000/7/31

2355 525300 Vehicle Maint-NY

Dr 400

73821 2000/7/31

2355 250000 Interco Payable-NY

Cr -400

...

.. |

This is classic intercompany accounting. It could be done

today. Setup

any big midrange accounting package that has a browser interface such as

Great Plains or Lawson. Sell subscriptions to a bunch of

companies. Establish a separate company in the system for each subscriber.

Then, create business objects to post each transaction event that happens between

subscriber companies to

the appropriate ledgers. The intercompany payables and receivables would

always agree, whenever both parties to any transaction happen to be your

subscribers. Perhaps some companies having strong integration needs might

subscribe to your service, such as supply chain partners.

Multi-company CDEA ledgers don't work out of the

box, however, because

- they impose a number of unnecessary structures on the parties, and

constrain their choice of software to a common platform.

- the "trusted third party" has way too

much access to all of your data,

- the processing of external transactions is too tightly coupled, for

example, requiring locks on your tables when 3rd parties conduct

business with you, and

- a classic multi-company ledger model maintains much more information

than that data which is truly common to both trading

partners. Maintaining two CDEA ledgers goes far beyond what is strictly necessary to achieve the objective of the shared

repository; for one example, every company has different charts of

accounts and other attribute tables which don't need to be on a shared

host.

- Business process is way too complex. To create correct

double-entry postings to every unrelated company requires knowledge

that only exists inside the companies not on the ASP

- Computer processing for a whole midrange/ERP system

is too great. Doesn't scale due to hardware costs.

- It is far too difficult to add new companies, and

each new company requires too much system resources.

- The model has no hope of widespread adoption.

Accordingly, the design for this STR is simpler --it models

only the

event of the completion, or execution, of a transaction.

This model stores the amount and other attributes as they were

agreed by two

parties, and of course, stores them only once rather

than in two ledgers as would be done in a multi-company ledger.

Theoretical basis for an STR model:

Classic double entry accounting (CDEA) is an ingenious

modeling language, having template or solution for any possible

transaction. All accounting systems in use today are CDEA

--even the list-oriented personal finance programs have "splits" in

which you classify your cash or investment movements into income, expense,

transfers, etc.

CDEA entries for external transactions (i.e.

involving other parties) are the focus of the STR. Half of the

any bookkeeping entry for purchases or

sales represents the money exchange versus the reciprocal party. The

other half of the entry, generally,

represents your internal classification as income, expense, inventory, or other asset

or liability. STR is not concerned with these classifications other than

to support them, and recommend they be classified with XBRL types.

The external date and amount agreed with trading partner, owner, debtor or creditor with whom

the business transaction was concluded, has always been recorded identically in the other party's

books. This will be shared in the STR. We are not breaking

any new ground in law or business culture.

Any

modernization of CDEA for the web must provide data structures that serve the

needs of both parties to the transaction. Existing B2B XML messages contain such

structures--they are event-oriented, single entry

accounting entries which identify both parties, and contain a

transaction date, amount, and list the products or services.

The global economy may be viewed as a 3-dimensional cube containing sheets for every party in the

universe, summing to zero. (More discussion at GLschema1,

GLschema2). The money movements

of the entire economy are a single, multi-company ledger.